Most financial crime doesn’t announce itself. It moves quietly through ordinary-looking transactions, unremarkable accounts, and clients who appear entirely legitimate on the surface. What breaks it open is rarely a dramatic confession or a lucky tip. It’s a pattern of signals that, once recognised, makes the suspicious activity impossible to ignore. That’s what AML red flags are: the early warning system that gives financial institutions the chance to act before real damage is done. And for institutions that take them seriously, that build the processes to identify, escalate, and act on them, they are genuinely one of the most powerful tools in financial crime prevention. Here’s a structured breakdown of what those signals actually look like across the categories that matter most. Read on to know the AML Red Flags every financial institution should watch for.

Why Red Flags Are Worth Taking Seriously

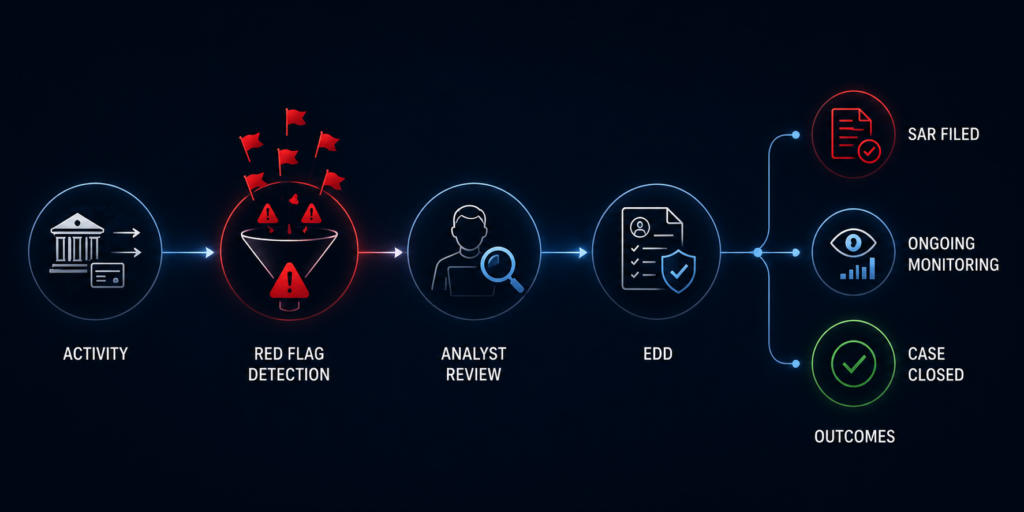

Before getting into the specifics, it’s worth being clear about what AML red flags are and what they aren’t. A red flag doesn’t prove a crime has been committed. It identifies where closer scrutiny is warranted.

That distinction is important, both for how institutions respond and for how investigators work with the information.

The practical value of a well-functioning red flag system is that it allows institutions to prioritise investigation resources toward the accounts and transactions that actually carry risk, rather than applying the same level of scrutiny uniformly across an entire customer base, which is neither practical nor effective.

The other thing worth understanding is that red flags are most powerful not as individual signals, but as converging patterns. A single indicator might have an innocent explanation. Two or three aligning around the same account or transaction tells a significantly different story.

Transaction Red Flags: Where the Money Tells the Story

Transactions are where financial crime most reliably leaves traces and where the clearest signals tend to appear. Structuring is one of the most well-documented patterns: breaking large sums into smaller deposits that fall just below mandatory reporting thresholds. The amounts themselves may look unremarkable. The pattern consistent, deliberate, repeated, is the flag.

Rapid movement of funds with no apparent business purpose is a reliable signal of layering activity. Money arriving and leaving within hours, across multiple accounts, with no commercial logic connecting the movement, is not normal business behaviour. It is the footprint of someone trying to put distance between funds and their origin.

Round-number transactions repeating at regular intervals are worth examining. Genuine commercial transactions are rarely this clean or this consistent. Regularity of this kind is a pattern, not a coincidence.

Wire transfers routed through unexpected jurisdictions or correspondent banks with no clear commercial rationale raise an obvious question: why this route? When there’s no answer that makes sense for that customer’s business, the routing itself becomes the flag. The key insight that experienced AML professionals apply here: it is not the size of a transaction that matters most. It is whether that transaction makes sense for that specific customer, at that specific moment in time.

A transaction that would be unremarkable for one customer profile can be highly suspicious for another.

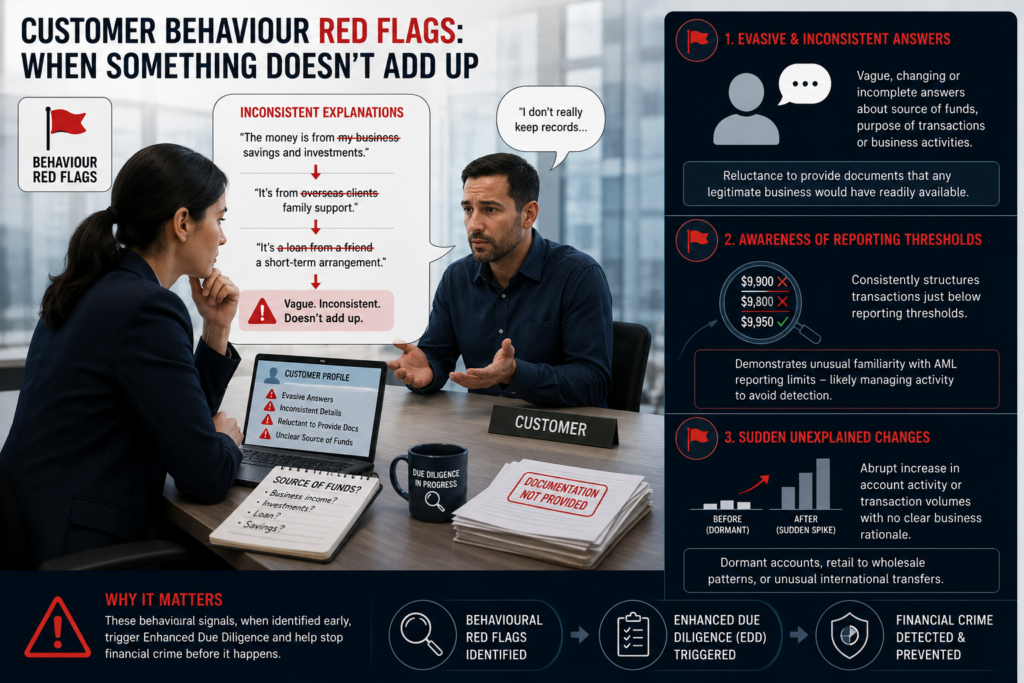

Customer Behavior Red Flags: When Something Doesn't Add Up

Some of the most telling signals come not from the transactions themselves, but from how customers behave when questioned about them.

Evasiveness about source of funds, purpose of transactions, or the nature of a business is a consistent precursor to financial crime. This is rarely outright refusal to answer, that would be too obvious. It’s vagueness that shifts and changes under follow-up questions. It’s answers that don’t quite fit together. It’s reluctance to provide documentation that any legitimate business would have readily available.

Customers who appear unusually familiar with AML reporting thresholds are signalling something. A customer who consistently structures their activity just below the thresholds that trigger reporting, and who demonstrates awareness of those thresholds in conversation, is not likely doing so by accident. This is one of the clearest behavioural signals that an individual is not just conducting transactions but managing them specifically to avoid detection.

Sudden unexplained changes in account behaviour warrant attention. A dormant account that suddenly receives large international transfers. A retail customer whose activity suddenly resembles a wholesale operation. A business account whose transaction volumes increase by an order of magnitude with no corresponding change in declared business activity. Normal accounts change gradually and for identifiable reasons. Abrupt, unexplained shifts in behaviour are not normal.

These signals, caught early, are exactly what triggers the enhanced due diligence that brings financial crime to the surface before it completes.

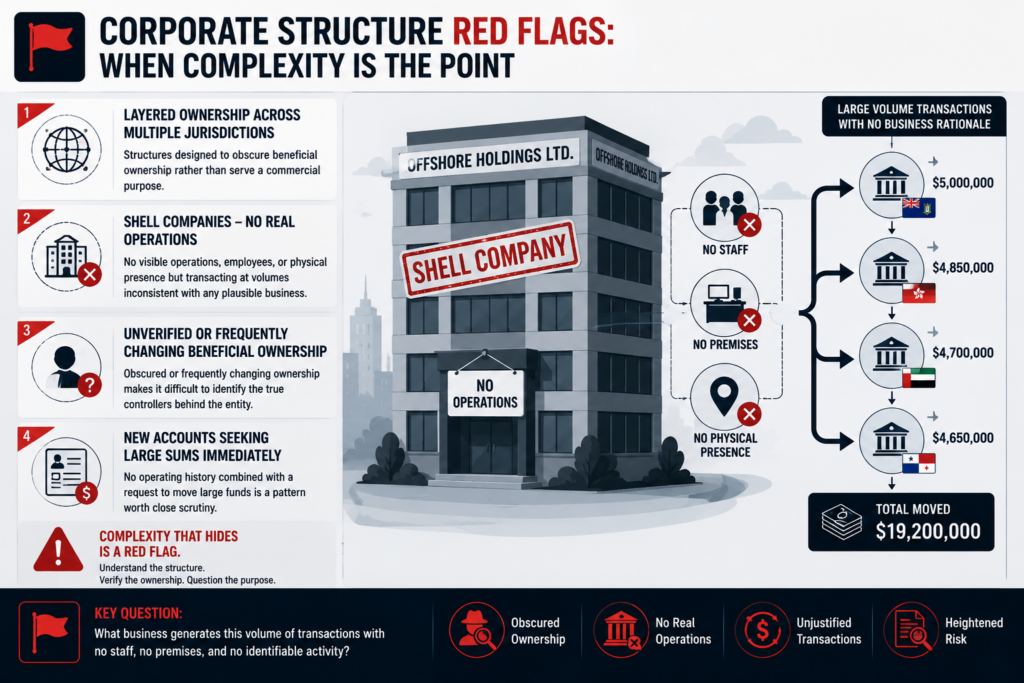

Corporate Structure Red Flags: When Complexity Is the Point

Legitimate businesses can have complex structures. But there’s a difference between complexity that serves a commercial purpose and complexity that exists specifically to obscure.

Ownership structures layered across multiple jurisdictions with no apparent commercial rationale fall into the second category. When a corporate structure appears designed to make beneficial ownership difficult to determine, rather than to serve any identifiable business function, that design is itself a red flag.

Shell companies with no visible operations, employees, or physical presence transacting at volumes inconsistent with any plausible business activity are a well-established vehicle for money laundering. The question to ask is simple: what business generates this volume of transactions with no apparent staff, no premises, and no identifiable commercial activity?

Beneficial ownership that cannot be confirmed, or that changes frequently without clear explanation, is a significant concern. FATF’s international standards require financial institutions to identify and verify the beneficial owners of legal entities specifically because this is where the connection between illicit funds and their true controllers is most often concealed.

New corporate accounts seeking to move large sums immediately, without any established operating history, combine two flags that individually might be explicable but together represent a pattern worth scrutinising closely.

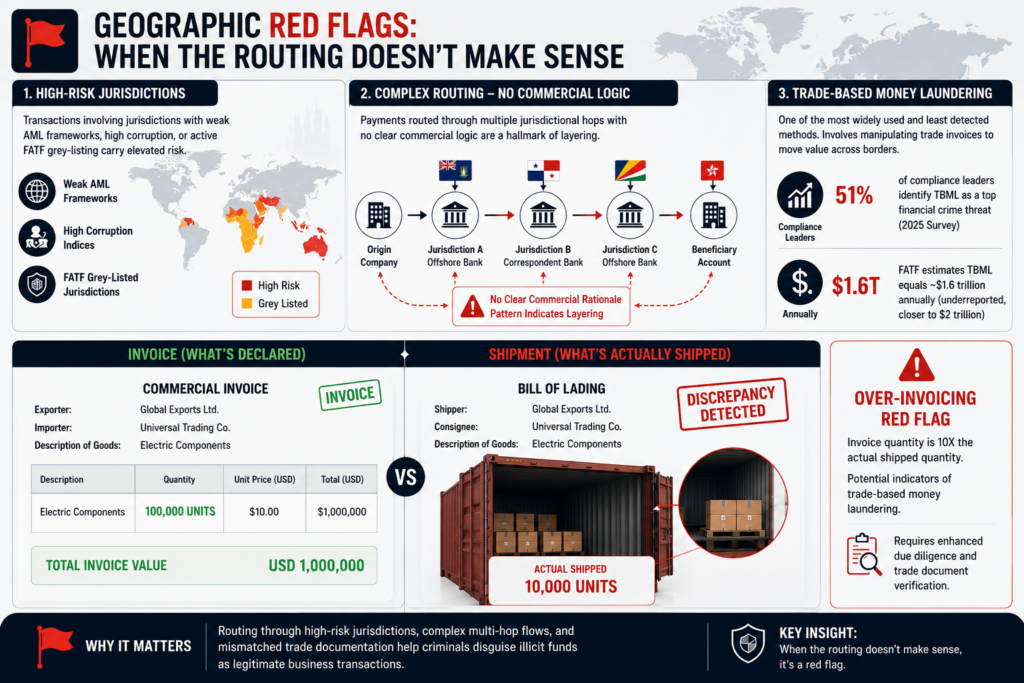

Geographic Red Flags: When the Routing Doesn't Make Sense

Geography matters in financial crime, not because crime is confined to particular regions, but because routing decisions reveal intent.

Transactions involving jurisdictions with weak AML frameworks, high corruption indices, or active FATF grey-listing carry elevated risk not because everyone transacting in those jurisdictions is a criminal, but because those environments offer less resistance to illicit flows. The presence of such jurisdictions in a routing pattern is a signal worth examining.

Payments routed through multiple jurisdictional hops with no clear commercial logic are a hallmark of layering. Funds moving from one country to another to another, through correspondent banks with no obvious commercial connection to the underlying transaction, are following a path designed to obscure, not to transact.

Trade invoices that don’t match the goods being shipped sit in a category of financial crime that is both widely used and significantly underdetected. In a 2025 State of Financial Crime Survey, 51 percent of compliance leaders identified trade-based money laundering as one of their top financial crime threats. FATF estimates that trade-based money laundering accounts for roughly $1.6 trillion annually, a figure already considered underreported, with some estimates placing it closer to $2 trillion.

Over-invoicing and under-invoicing on international transactions, inflating or deflating the stated value of goods to move funds across borders under the cover of legitimate trade, is one of the most widely used and least detected laundering methods in operation today.

The reason it persists is precisely because it embeds illicit flows within legitimate-looking trade transactions, making detection dependent on cross-referencing financial data with trade documentation, a step many institutions are not yet doing systematically.

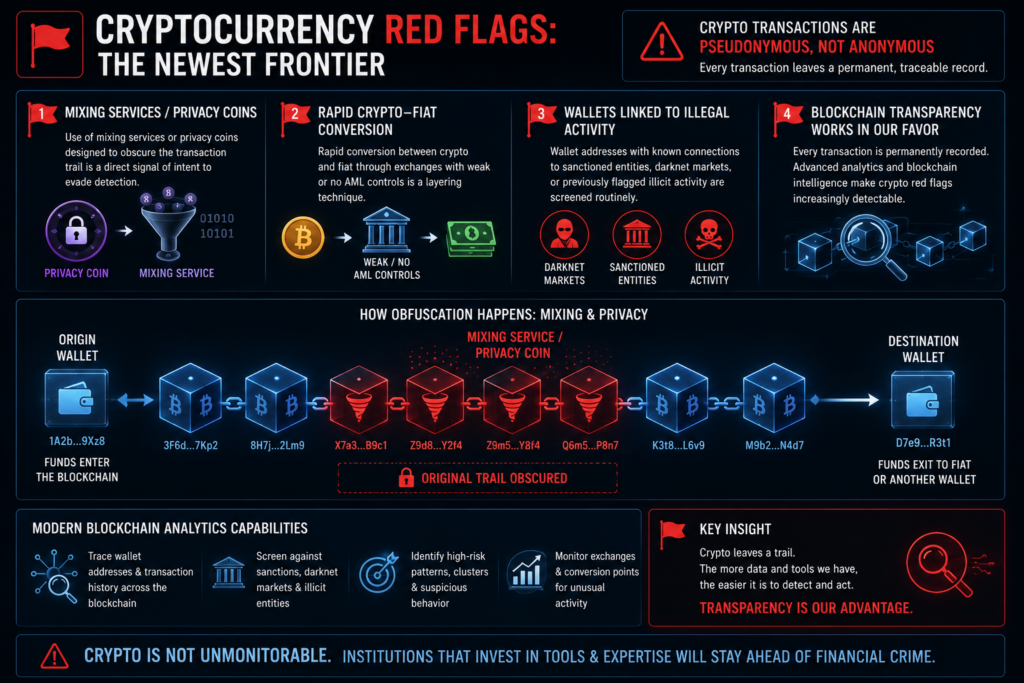

Cryptocurrency Red Flags: The Newest Frontier

Cryptocurrency has introduced a new category of red flags that financial institutions are increasingly expected to understand and monitor, and the good news is that the tools to do so are developing rapidly.

Use of mixing services or privacy coins specifically designed to obscure the transaction trail is a direct signal of intent to evade detection. While there may be legitimate privacy motivations for such tools in some contexts, their use in financial transactions involving institutions warrants scrutiny.

Rapid conversion between crypto and fiat through exchanges with weak or no AML controls is a layering technique, using the conversion process to break the link between the original funds and their destination in the conventional financial system.

Wallet addresses with known connections to sanctioned entities, darknet markets, or previously flagged illicit activity are now screened routinely by institutions with access to blockchain analytics tools. These tools allow institutions to screen wallet addresses and trace transaction histories in ways that were not possible even five years ago, crypto red flags are increasingly detectable, not less so.

The trajectory here is encouraging. The blockchain’s fundamental transparency, the fact that every transaction is permanently recorded and publicly visible, means that the investigative tools available to institutions and investigators improve with every year.

Financial crime that moves through cryptocurrency leaves a trail. The institutions that invest in the tools and expertise to read that trail are significantly better positioned than those that treat crypto as an unmonitorable frontier.

The Practical Takeaway

Red flags don’t tell you what is happening. They tell you where to look. The institutions that build robust red flag monitoring that invest in the systems, training, and investigative capacity to act on what those systems surface, consistently catch financial crime earlier, file better Suspicious Activity Reports, and build the kind of compliance record that regulators recognise as genuine effort rather than a checkbox exercise.

FATF’s standards require continuous transaction monitoring, not periodic reviews, but ongoing analysis that compares transactions against customer risk profiles and flags deviations for investigation. Institutions that treat this as a live, active process rather than a retrospective audit are operating at the level the threat environment actually requires.

The difference between catching financial crime at the first red flag and catching it six months later is measured not just in investigative complexity, but in recoverable funds, reputational exposure, and regulatory consequence. The signals are there. The question is whether the institutions looking at them know what they’re seeing, and what to do next.

FAQs

What are are AML red flags?

AML red flags are a signal or pattern of behaviour that indicates a transaction or account warrants closer scrutiny. It does not confirm criminal activity, it identifies where enhanced due diligence is needed. Red flags are most powerful when multiple indicators align around the same account or relationship.

What happens when a financial institution identifies a red flag?

Identifying a red flag triggers a review process. Depending on the institution’s risk framework and the nature of the signal, this may involve enhanced due diligence, customer questioning, internal escalation, or the filing of a Suspicious Activity Report (SAR) with the relevant financial intelligence unit.

What is structuring, and why is it an AML red flag?

Structuring, also known as smurfing, is the practice of breaking large sums into smaller transactions that fall below mandatory reporting thresholds, specifically to avoid triggering those reports. The individual transactions may look unremarkable. The pattern of deliberate, repeated sub-threshold activity is the flag.

What is trade-based money laundering and why is it so hard to detect?

Trade-based money laundering involves disguising illicit funds within legitimate trade transactions, typically through over- or under-invoicing, false shipment documentation, or phantom shipments. It’s difficult to detect because it embeds illicit flows within high-volume, complex, cross-border trade activity. Detecting it requires cross-referencing financial data with trade documentation, which many institutions are not yet doing systematically.

How are cryptocurrency transactions monitored for AML purposes?

Blockchain analytics tools allow institutions to screen wallet addresses against known illicit actors, trace transaction histories, and identify connections to sanctioned entities, darknet markets, or previously flagged activity. The permanent, public nature of blockchain data means that cryptocurrency transactions leave a traceable record and the tools to read that record are improving rapidly.

What is the difference between AML red flags and a Suspicious Activity Report?

AML red flags are signals that triggers review. A Suspicious Activity Report is the formal document filed with a financial intelligence unit when an institution, after investigation, believes a transaction or pattern of activity may involve financial crime. Not every red flag results in a SAR but every SAR should have been preceded by the identification and investigation of red flags.

How does CAT Investigators support financial institutions with AML?

CAT Investigators provides financial crime investigation, due diligence, and asset tracing services to financial institutions, legal teams, and compliance functions. Where internal monitoring surfaces signals that warrant deeper investigation, particularly involving complex corporate structures, cross-border activity, or cryptocurrency, we provide the investigative capacity to go further than internal teams typically can.