The UK FATF presidency opened with a global fraud summit‑style webinar that sets out how quickly money moves, how slowly most systems respond, and what has to change in financial intelligence and asset recovery.

On paper, the event was a webinar: the first public meeting under the UK presidency of the Financial Action Task Force. In practice, it felt closer to a strategic launch.

Instead of starting with a plenary on mutual evaluations or virtual assets, FATF chose to put fraud at the centre and used the session to outline a two‑year roadmap, complete with hard timelines and specific focus areas.

The UK president opened by stating that the new presidency has three priorities: fraud, a sharper implementation of the risk-based approach, and improved information sharing to tackle financial crime. That choice reflects pressure from multiple sides. Stakeholders across the FATF network have been asking the organisation to “do more on fraud”, and the data supports their concern. The opening remarks cited an estimated global fraud cost of about 500 billion dollars a year and noted that fraud is the predominant predicate offense in around 90% of FATF mutual evaluations. This is not a marginal threat. It is the main driver behind most modern money‑laundering cases assessed in the last round.

The president also acknowledged a structural problem. FATF’s standards were built on a “follow the money” logic that traditionally focused on laundering after a predicate offense. Fraud does not fit neatly into that sequence.

In many cases, the laundering of fraud proceeds is intertwined with the commission of the fraud itself – money moves across borders and into virtual assets in three minutes, not weeks. Treating fraud as just another predicate, or as a side‑branch of cybercrime, no longer works.

Why fraud moved to the top of the FATF agenda

Victims, scam compounds and national security.

One of the more striking elements of the webinar was its tone. FATF often speaks in terms of “risks” and “threats”; here, the UK presidency started with victims. It emphasised individuals who lose their life savings and the less visible group of people trafficked into scam compounds, held in conditions resembling modern slavery and forced labour to run fraud operations. That human‑level description framed fraud as more than an economic nuisance. The remarks explicitly linked fraud to financial stability, financial inclusion and national security for many member countries.

The focus on scam compounds is not cosmetic. FATF plans to spend the period up to October concentrating on these facilities, drawing on work already done by the UN, Interpol and regional bodies such as APG and AAMS. The aim is to move quickly from “admiring the problem” to mapping detection and disruption techniques, identifying gaps and agreeing potential actions. The presidency made clear that this is a first phase:

- Up to October: Concentrating on scam compounds to map detection and disruption techniques.

- October to February 2027: Widening to cyber-enabled fraud more broadly, producing a picture of good practices and systemic gaps.

- February 2027 to June 2028: Shifting to implementation, using FATF’s assessments and follow-up processes as levers.

A roadmap built on existing FATF tools

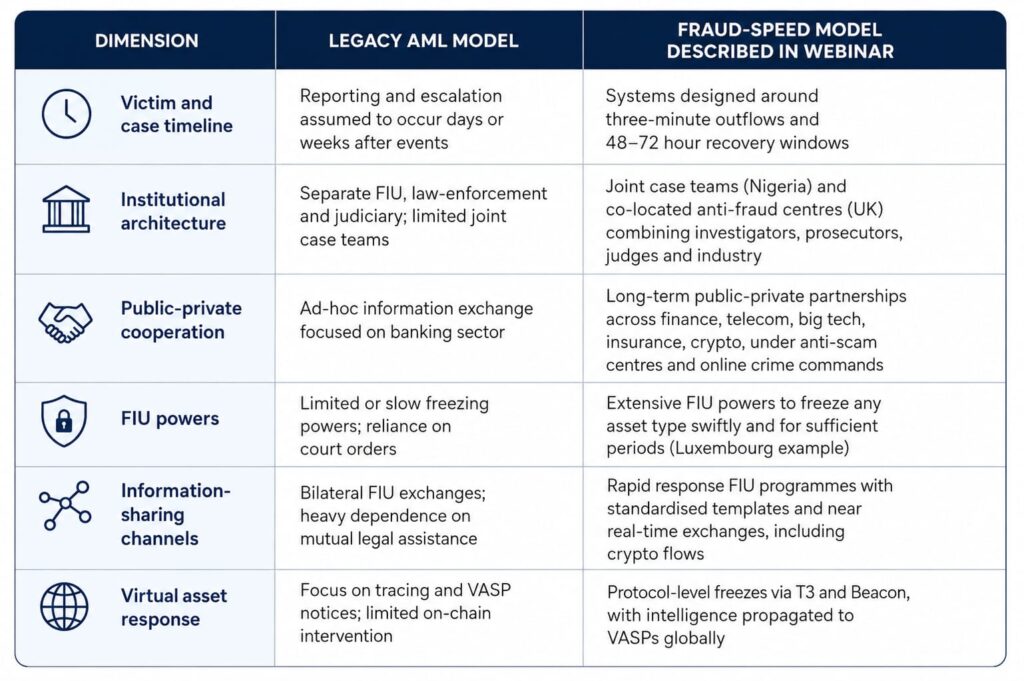

The secretariat’s intervention underlined that the fraud roadmap is not about inventing entirely new standards. It is about using existing ones for a different purpose. Payment transparency-where standards have already been updated is meant to improve traceability and visibility of the payment chain, which directly affects fraud detection. Regulation and supervision of virtual assets are intended to close gaps that allow fraudsters to exploit crypto both to commit fraud and to launder proceeds.

Asset recovery tools already exist, including powers to freeze and confiscate criminal proceeds and, in some cases, to act without a prior conviction, supported by stronger international cooperation. Beneficial‑ownership transparency and digital ID guidance aim to make it harder for fraud networks to hide behind complex structures or false identities. FATF has also invested in partnerships with organisations such as Interpol and the Egmont Group on cyber‑enabled crime. The roadmap’s ambition lies in accelerating and re‑targeting this toolkit towards fraud, not in replacing it.

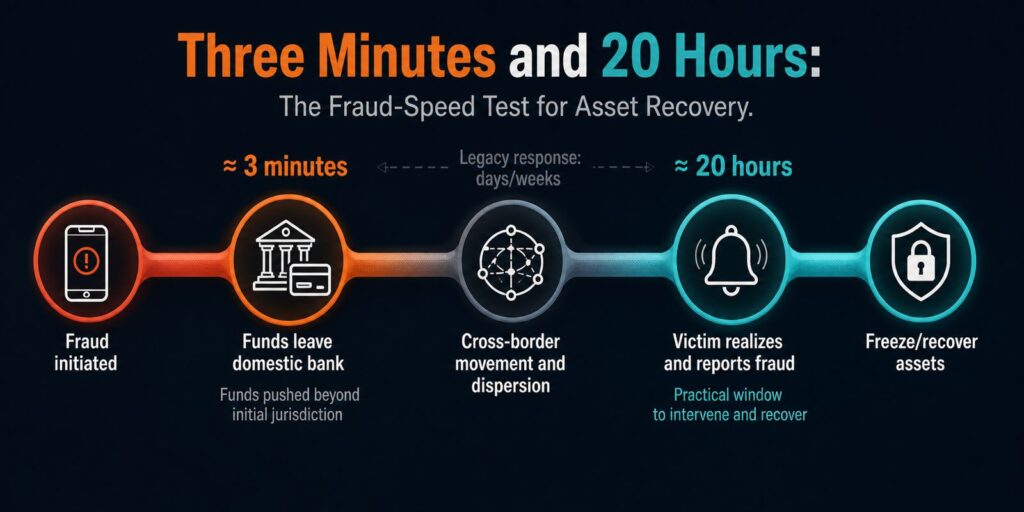

The numbers that defined the webinar: three minutes versus 20 hours

Thailand’s whole‑of‑country approach and the prevention gap

The first panel, on “rethinking financial intelligence”, was where the webinar shifted from policy to operational detail. Thailand’s representative described new cyber‑fraud legislation that enables a whole‑of‑country approach. In this framework, all relevant actors – telcos, social media platforms, banks, payment providers, digital‑asset firms, regulators, police and government agencies are bound into a single system. Roles for each party are clearly defined, information sharing is allowed, and incentives and disincentives are spelled out in what was described as a “shared responsibility” framework.

The most arresting part of Thailand’s intervention was the data. Once a victim transfers money to a fraudster, around 50% of the loss can be out of the country within three minutes. On average, victims become aware that they have been scammed approximately 20 hours later. Those two numbers three minutes and 20 hours capture the core mismatch FATF is trying to address.

Many AML processes still assume that reporting, analysis and escalation can occur at human speed. Fraud operates at network speed. Thailand’s conclusion is that the country needs to move from reacting to preventing, and that AI will be central to moving detection and intervention into that three‑minute window.

Nigeria’s national security lens and joint case architecture

Nigeria’s contribution showed what happens when fraud is treated as a national‑security issue rather than a routine economic crime.

The government has placed the fight against scams and fraud “at the apex of the political agenda” and has framed it as a non‑negotiable national security imperative. That framing has practical consequences. Law‑enforcement efforts have been ramped up through a multi‑agency approach that is heavily intelligence‑led, driven by increased financial intelligence from the NFIU to law‑enforcement agencies.

The outcomes are concrete. Nigeria has arrested more than 792 people in connection with scam operations, including 192 foreign nationals running scam centres out of Lagos. These actions include asset recovery, cross‑border operations and technical cyber‑threat mitigation. Institutional changes underpin those numbers. A joint case team on cybercrime, coordinated under national‑security structures and operating within the Ministry of Justice, brings together investigators, prosecutors and judges to handle online fraud cases.

Additional initiatives include information sharing of threat intelligence with the FIU and leveraging bilateral agreements particularly with the UK to run joint fraud actions focused on intelligence sharing, capacity building and public awareness.

For readers, this is more than a set of statistics. It illustrates how political prioritisation, FIU empowerment and joint case architecture can convert financial intelligence into arrests and asset recovery rather than allowing it to stagnate as reporting.

Collapsing detection‑to‑action time: anti‑scam centres and FIU rapid response

UK anti‑fraud centres and the online crime command

The UK panellist framed fraud through the lens of institutional design. Around the world, an increasing number of countries have set up anti‑scam or anti‑fraud centres as national responses. These centres are often co‑located and multi‑agency, built on public‑private partnerships that compress the time between detection and action. Financial intelligence has shifted from static reports towards operational, real‑time data in bank accounts and across sectors.

In the UK, a ten‑year history of public‑private partnerships with the financial sector laid the groundwork. Intelligence sharing and shared risk mapping have evolved into structures that now include wider policing, security services and key industry sectors such as finance, telecom, big tech, insurance and crypto.

The recently announced online crime command, part of the country’s fraud strategy, builds on this model. It convenes different sectors to unite data, expertise and operational capability in one place, rather than relying on ad‑hoc cooperation.

The panel suggested that FATF could help scale these models internationally by facilitating peer‑to‑peer learning on public‑private partnerships and, more interestingly for practitioners, by crediting effective anti‑scam centres in mutual evaluations. That would create a direct incentive for other jurisdictions to invest in similar architectures.

FIU‑to‑FIU rapid response and freezing powers

The webinar also introduced a more specialised tool: a rapid response programme among financial intelligence units. The idea is to move beyond slow, bilateral exchanges towards near real‑time sharing of precisely calibrated information. FIUs agree on standardised procedures and templates that deliver exactly what counterparts need to trace fraud proceeds – no more, no less.

A case study brought this to life. Fraud proceeds moved from a bank in one jurisdiction to a bank in another, then into a crypto‑asset service provider where part of the funds was converted into crypto. Within days, FIUs and obliged entities traced those flows and managed to freeze both fiat and crypto funds. This outcome depended on three conditions: obliged entities (banks and VASPs) fulfilled their roles and reported suspicious activity; FIUs could exchange information swiftly under the rapid response arrangements; and FIUs had legal powers to freeze assets promptly and for a sufficient period to allow judicial authorities to recover funds.

Luxembourg’s FIU highlighted its own extensive freezing powers, which allow it to act quickly on any type of asset, including crypto, and to hold those assets long enough for international cooperation and judicial processes to run their course.

The broader message was clear. Having rapid response channels and freezing powers on paper is one thing; using them consistently and correctly is another. Awareness, procedure updates and close cooperation between FIUs, obliged entities, law‑enforcement and judicial authorities are essential.

Fraud in crypto: from tracing to “public‑private disruption”

T3, Beacon and freezing at protocol level

The webinar’s most forward‑leaning segment came from TRM Labs, which discussed asset recovery when fraud proceeds move into virtual assets. Traditional tools often operate on fiat rails and depend on correspondent banking relationships or banks at the other end that can act on messages. Crypto, by design, is borderless. A transaction confirmed in Brazil can settle in Singapore in seconds; there may be no bank to call and no wire to stop.

To address that gap, TRM Labs described two initiatives: the T3 financial crime unit and the Beacon network. T3 is a partnership between TRM Labs, Tether and Tron. It is designed to support law‑enforcement investigations by enabling partners to freeze funds directly on‑chain at protocol level in real time when a freeze request comes in. Beacon complements this by propagating related intelligence to virtual‑asset service providers globally so they can identify and block attempts to cash out.

The results presented at the webinar were significant. Combined, T3 and Beacon have helped freeze over half a billion dollars in illicit funds across multiple blockchains and more than 20 jurisdictions. Response times have dropped from days to hours, and sometimes to minutes, including cases where funds were frozen even before victims filed formal reports. TRM described this as “public‑private disruption” a shift from partnership as information exchange towards partnership as coordinated, real‑time intervention.

For investigators, prosecutors and compliance officers, this segment of the webinar signals that asset recovery in crypto is no longer limited to forensic tracing and slow judicial processes. Under the right conditions, it can involve rapid network‑level freezes that materially change recovery prospects.

What happens next: FATF’s convening power and the global response against fraud

The closing remarks pulled the webinar’s threads into a clear next‑steps roadmap.

FATF will not start by rewriting its standards. Instead, it will push countries to use existing tools more aggressively against fraud payment transparency, virtual‑asset regulation, asset‑recovery powers, beneficial‑ownership transparency and digital ID guidance and will recalibrate evaluations, follow‑up and policy work so performance on fraud becomes a visible test of AML/CFT effectiveness.

To make that summit more than another talking shop, FATF signalled three practical aims:

- Pinpoint where it can add the most value by helping scale successful models – anti‑scam centres, FIU rapid‑response programmes, protocol‑level freezes, and whole‑of‑country approaches like Thailand’s.

- Use its assessment and follow‑up powers to nudge supervision and incentives so meaningful participation in high‑value public‑private initiatives is recognised, not treated as optional.

- Anchor future guidance and peer reviews in what demonstrably improves recovery rates within the 48-72 hour window that matters for fraud.

For practitioners reading this, the fraud roadmap is not just another checklist item. It is the lens through which FATF will increasingly judge whether a country’s AML/CFT regime delivers real‑world impact.

The “three minutes and 20 hours” insight from Thailand has become more than a striking statistic; it is a benchmark for whether intelligence, legal powers and public‑private cooperation are aligned with the speed of modern fraud.